U.S. Community Investing Index

Overview

The U.S. Community Investing IndexTM (“USCII” or “the Index”; Bloomberg Ticker: CMTYIDX) is an index of publicly traded companies designed to identify those that contribute positively to the communities in which they source, operate, and sell.

Heron developed the index in 2005 to understand how large companies contribute to (or detract from) Heron’s mission to help people and communities help themselves out of poverty. Over the past decade, Heron and its research partners have refined the methodology to draw from new data sources and better align the index with Heron’s strategic objectives.

History

Heron and its research partners used a rigorous methodology to identify companies that contribute positively to the communities in which they source, operate, and sell. The positive screen was organized around the capitals of Heron’s net contribution lens. Heron worked with custom data and research providers to evaluate the impact of companies on stakeholders within these capitals.

| Capital | Stakeholder | Hypothesis & Evaluation Criteria |

|---|---|---|

| Human | Employees

Suppliers | Hypothesis: One of the most direct opportunities for companies to impact society is through their employees.

Evaluation criteria include: Pay & benefits, work-life balance, health & safety, training & education, strategic training management, equal opportunities & non-discrimination, broad-based employee ownership Hypothesis: Companies increasingly rely on supply chain partners to outsource low-wage work. Evaluation criteria include: Transparency & performance related to supply chain labor including human rights, health and safety, freedom of association, forced labor |

| Financial | Board & Investors

Management | Hypothesis: Management of impact comes from the top. Governance and ethics protocols influence a company’s ability to manage and optimize for social and financial performance.

Evaluation criteria include: Governance & ethics, board diversity/independence, pay distribution, shareholder democracy, accounting policies Hypothesis: Management will be better suited to manage a company’s impact on its stakeholders if incentive structures are aligned with long-term value creation. Evaluation criteria include: Integration of sustainability performance objectives into the variable remuneration of members of the executive management team |

| Civic | Government

Customers

Neighbors | Hypothesis: Companies impact their communities both positively and negatively by interacting with local and national governments. Interactions often include paying taxes, receiving subsidies, and lobbying.

Evaluation criteria include: Taxes and subsidies, presence in jurisdictions enabling tax-base erosion and profit-shifting; controversies related to tax avoidance, political contributions & lobbying. Hypothesis: Companies impact customers through their products and services. Evaluation criteria include: Product safety, responsible marketing, pricing & affordability, product-related controversies Hypothesis: Neighbors include stakeholders who aren’t necessarily employees or users of products and services. Companies impact neighbors directly through operations and indirectly through sourcing practices. Evaluation criteria include: Community involvement, monitoring and evaluation of community projects, community outreach and consultation, human rights practices & results. |

| Natural | Environmental inputs

Environmental outputs | Hypothesis: Companies have an impact on the environment through the sourcing and management of their production inputs.

Evaluation criteria include: Environmental management in the supply chain, sustainable procurement of supplies and/or raw materials used for production. Hypothesis: Companies have an impact on the environment through their operational outputs, as well as through their products and services. Evaluation criteria include: Environmental management, climate change strategy, eco-efficiency, product lifecycle |

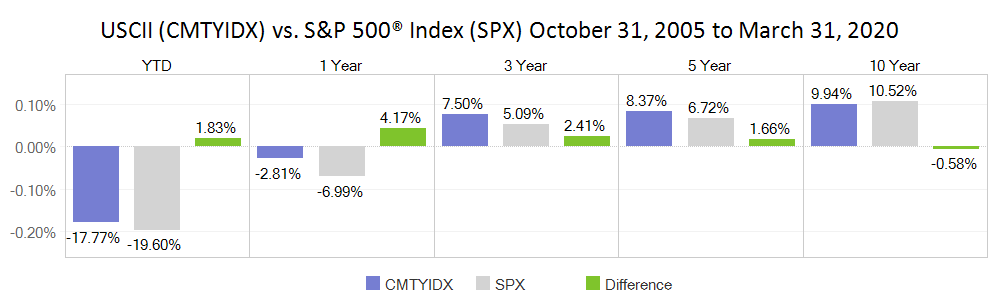

Index Performance

Process

Index Creation

Heron was responsible for selecting securities in the index, and it does so by compiling a positive screen using the four capitals and their underlying stakeholders.

Heron used absolute weighting coefficients at the capital level:

- 30 percent: Human Capital (including employees and suppliers)

- 30 percent: Civic Capital (including government, customers, and neighbors)

- 20 percent: Natural Capital (including environmental inputs to and outputs from production)

- 20 percent: Financial Capital (including the board, management, and investors)

Heron then dynamically weighted stakeholder scores depending on what is relevant to any given industry.3 For example, suppliers could have represented between 10 percent and 60 percent of the Human Capital score, depending on how heavily the company relies on outsourced labor. The industry-relative stakeholder weighting coefficients were informed by Heron’s research partners.

Each company is scored between -5 and +5, and companies that score a 0 or higher were then considered for inclusion in the index.

The selection universe was then run through a rules-based “reality check” that looks for additional controversies that are deemed very severe. These controversies could have been over- or under-expressed in the scoring process due to timing, score weighting, or other factors. The reality check was conducted quarterly and reviewed by Heron’s staff and the USCIITM advisory committee.

The USCIITM was then constructed using a free-float-adjusted market-capitalization weighting methodology, managed by S&P Dow Jones Indices.

Index Monitoring

The U.S. Community Investing IndexTM was overseen by an advisory committee of professionals in pertinent fields, including but not limited to sustainable investing, philanthropy, and social data. The advisory committee met quarterly with Heron staff and research partners to discuss methodology enhancements and review index performance.

[1] The U.S. Community Investing Index (the “Index”) is the property of Heron. The Index is not sponsored by S&P Dow Jones Indices or its affiliates or its third-party licensors (collectively, “S&P Dow Jones Indices”). S&P Dow Jones Indices will not be liable for any errors or omissions in calculating the Index. “S&P Dow Jones Indices” and the related stylized mark(s) are service marks of S&P Dow Jones Indices and have been licensed for use by the F.B. Heron Foundation. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (“SPFS”), and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”).

[2] The methodology management and maintenance relied on custom research partnerships with oekom research AG and the National Center for Employee Ownership (NCEO).

[3] Capital coefficients were consistently applied to all companies/industries (Human 30%, Civic 30%, Natural 20%, and Financial 20%). Stakeholder coefficients relied on the industry-relative stakeholder materiality assessment conducted by oekom research AG, so it varied by company.