Conscious Portfolio Construction

Table of Contents

Examining the Portfolio through an Enterprise Lens

Impact Everywhere

– Beyond Risk & Return

– Asset Class Highlight: Public Equities

Lessons Learned the Hard Way

Moving Forward

Examining the Portfolio through an Enterprise Lens

Heron began its mission-related investing efforts in 1997. At the time, some mainstream critics believed that seeking impact with the whole portfolio would depress financial returns and perhaps even cause Heron to shrink over time. Despite these criticisms, Heron invested about 40% of its assets for mission, and remained at 40% for a number of years.

In 2012, Heron ramped up this work and committed to investing 100% of its assets in better alignment with its mission. Heron’s decision to pursue a mission-aligned portfolio, what we think of today as a “conscious portfolio,” was and remains undergirded by a focus on the impact of specific enterprises (as opposed to industries, asset classes, investment vehicles, or other common thematic groupings). This reflects our belief that every enterprise has a variety of impacts through its business and operations (both positive, like hiring workers and paying taxes, and negative, like polluting the environment or ignoring exploitation in their supply chain).

Upon making that commitment, we began to examine our portfolio to find out what enterprises we owned in the “unscreened” 60% of assets. The Portfolio Examination Process (or PEP) combined a general measure of each enterprise’s standing on economic, social and governance (ESG) metrics with a particular measure of how many jobs an enterprise was providing.

Unfortunately, starting with a preferred metric and applying it to the entire portfolio didn’t quite render the results we hoped for. For example, it turned out that focusing solely on the number of jobs provided (even jobs providing opportunity in low-income areas) could have made a private prison company a darling among the REITs in our portfolio. We also discovered that many enterprises appeared both in the mission-screened and “non-mission” portions of our portfolio, which called into question how we were categorizing our investments, and underscored the (positive and negative) impacts had by all enterprises.

PEP revealed the value of a discovery process that was less prescriptive and more exploratory. Our experiences with PEP, and in particular the mistakes we made, taught us to “broaden our aperture” and look at our investments with a view to overall impact first, rather than a narrow lens of one particular kind of impact — an approach we now refer to as the “net contribution” lens.

Back to top

Impact Everywhere

Every investment has impact, so Heron does not limit its investment universe to just a few asset classes or types of enterprise. By using an array of financial tools, we support a diverse group of enterprises (including nonprofits, for-profits, and government entities). This helps us minimize risk, optimize liquidity, manage transaction costs, and maintain the flexibility required to provide communities with the types of capital they identify as most helpful.

Our direct investments generally take the form of grants, which we try to structure in a way that supports the health of nonprofit enterprises. By doing most of our nongrant investing indirectly through financial intermediaries, we can help capitalize a larger number of enterprises. We are also able to learn alongside our managers as the practice of impact investing matures.

Beyond Risk and Return

Like any investor, we weigh the merits of each investment carefully. Some of these characteristics may seem relatively familiar to traditional investors, such as risk and return profiles, liquidity options, and time horizon. But as a mission-oriented investor, we also weigh other factors that traditional investors leave out, including how a company treats employees, manages waste, and impacts the communities in which it operates. And as a philanthropic investor, we sometimes choose to make investments for which we expect a below-market rate of return because we have a compelling mission-related reason for doing so (and we designate such investments as “program-related investments”).

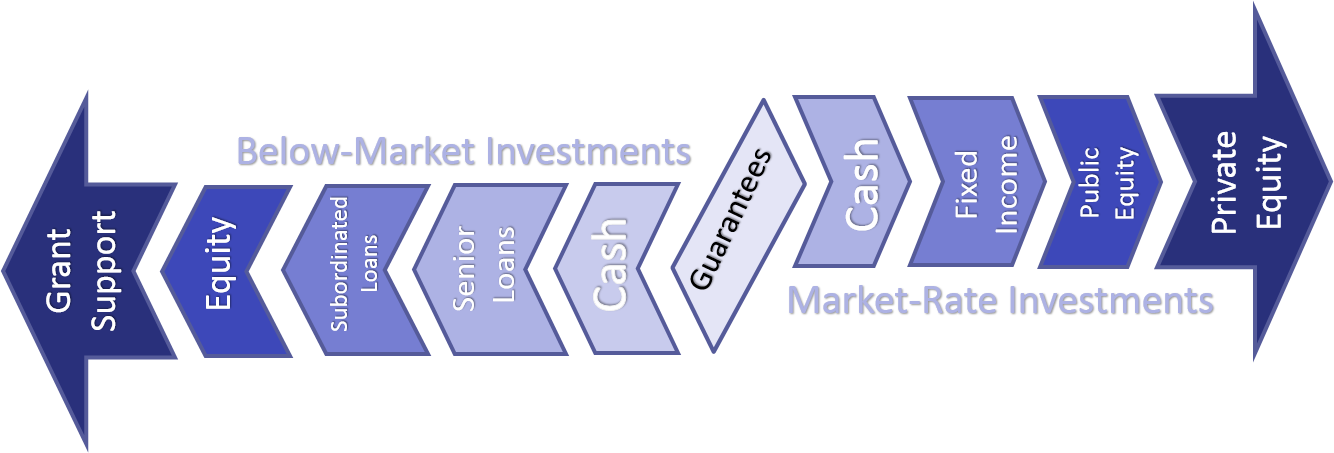

The graphic below illustrates the spectrum of investment tools that Heron utilizes to make both market-rate and below-market investments, from low-risk guarantees in the center to “high-risk” (from a financial standpoint) investment types on either end:

Note that this graphic only looks at the risk and return expectations for a variety of investments that a conscious investor might make. In reality, every investment provides a different set of considerations, including (but not limited to) risk and return profiles, liquidity, financial diversification compared to your existing portfolio, the types of expected impact, degree of visibility to (or data about) impact, and breadth of the impact across a number of people or a geographic area.

Asset Class Highlight: Public Equities

Serving our mission through a variety of investing approaches can apply even within a single asset class. For example, in our public equities, Heron’s U.S. Community Investing Index aims to identify companies that are “best in class” contributors to communities across the United States within a particular universe of companies. Another investment, Ownership Capital, takes a different approach to portfolio construction — one portion is composed of companies that are actively counseled to become better corporate actors, while the other portion is composed of best-in-class companies.

Back to top

Lessons Learned the Hard Way

Looking back to the steps Heron took before, during and since our Portfolio Examination Project affirmed some aspects of our approach; other aspects we would shed or adjust.

- DO know what you own. Our experiences have affirmed the value of working with managers, custodians and advisors to understand the totality of the enterprises in the portfolio.

- DON’T try to shoehorn all of your investments into a single data source, or measure them all by the same kind of data point (like we did with “number of jobs”).

- DO work with your advisors and managers to find out what you can find out. Seek out what data is available about those investments, and look at what those data sets reveal. Part of Heron’s journey included the discovery that many companies included in the mission portfolio were selected based on ranking well on metrics such as corporate philanthropy, but we felt that their actual business practices were detrimental to communities we cared about. This fed some rich conversations with our data providers and ultimately drove us to rethink some of our screening processes.

- DON’T rely too heavily on the data without understanding the processes, choices, collection methods and assumptions that went into it (and how the data provider processes “nulls” or bald spots in the data). Instead, seek out the stories behind the data, and (to the degree they are available), the stories that make sense of a variety of data points. For example, we found that a Europe-based data provider scored job quality and benefits differently than an American provider, based on assumptions about the healthcare provided by developed countries. When doing deeper dives into particular investments, we might search out a variety of information sources to paint a fuller picture, from online reviews to local news articles or even city council minutes.

- DO thoughtfully marry the qualitative and quantitative. Taking a deeper look at anything that is surprising and/or doesn’t align with expectations is an important part of the process, and a rich opportunity for learning more and defining values. Surprises for us included things like:

- An unexpected concentration of scores (such as when very different bonds all received the same rating because they were issued by the same enterprise)

- Misalignment between two impact data providers on the same enterprise — a common occurrence, in part because not every data set reflects the same facts or value judgments

- Controversy at an otherwise positively-screened enterprise.

- DON’T limit yourself to only one approach. We now use different areas of the portfolio as different learning opportunities. This helps in figuring out our comfort level with the data we are getting, and in refining the metrics, values, or lenses we are applying to our portfolio as a whole. Even within our public equities portfolio, we find that different lessons come from developing our own index (the U.S. Community Investing Index™), and working with managers with different screens and approaches (such as Aperio and Blackrock).

- DO engage in ways that make sense for you. For some investors, or some investments, the best way to “engage” with enterprises that don’t live up to certain standards is to divest — and our belief that we are complicit in what we own sometimes leads Heron to do so. Other times, various kinds of engagement are appropriate. Our manager Ownership Capital explicitly invests in a small number of corporate entities that have expressed openness to change, and helps them move up the curve to more positive impact. Sometimes Heron has the opportunity to engage with enterprises in our sphere to encourage certain changes. Other investors have a strong focus on proxy voting and corporate activism to encourage the changes they wish to see.

- DO evaluate your managers based on their demonstrated alignment with the values and impacts you would like to see in your portfolio.

Moving Forward

Just as no investor ever stops optimizing for financial performance, Heron will also never stop optimizing our portfolio to better serve our mission.

Part of the impetus for that journey was our conviction that Heron and others can look at the impact of an entire portfolio, and optimize for it, while making similar or better risk-adjusted returns. Today, we see a market that is no longer mired in the belief that having a positive impact requires accepting lower returns, but rather, has ample data to encourage continued growth in the practice and development of impact investing.

As a result, we feel an increased sense of freedom to take on new and different kinds of risk in pursuing our mission to help communities help themselves with both our investment portfolio and our overall portfolio of work. We are now turning our attention to rotating to a portfolio comprised of investable opportunities that, on the whole, directly impact communities we are active in for the better.

Over the coming 8 years, Heron will shift the lion’s share of its investable portfolio to Community Capitals Partners in the form of major grants. During this transition, we will manage a substantial but declining investable asset base (currently $330 million) and identify the assets to populate a smaller (roughly $80 million) core investable portfolio to sustain its continuing operations. Initially, Heron will seek marketable investments that promise community benefit and feature liquidity.

Simultaneously, we will begin shifting our investable portfolio to direct community investments, prioritizing communities where Heron’s community program strategy is active in. In particular, Heron will seek out equity and debt investments that enable local development entities to expand their capacity to steward regenerative capital for their communities. Throughout this transition and beyond, Heron will continue to align all of its investments with its mission and will use Net Contribution expectations to guide decision-making. Should Heron be successful in this transition, we hope to serve as an example for institutions with significant financial capital that have expressed commitment to mission investing, especially for those with a place-based focus.